Have you ever spotted a charge on your credit card statement labeled “Ibila” and wondered what it means? If so, you’re not alone and it’s important to understand what this charge represents before it affects your finances.

Whether it’s a legitimate purchase, a subscription fee, or something unexpected, knowing how to identify and handle the Ibila charge can save you time, stress, and even money. You’ll discover exactly what the Ibila charge is, why it might appear on your credit card, and the steps you should take if you don’t recognize it.

Keep reading to take control of your credit card statement and protect your financial peace of mind.

Ibila Charge on Credit Card Explained

Seeing an Ibila charge on your credit card can cause confusion. Many people do not know what it means or why it appears. This section breaks down the Ibila charge and its common causes. Understanding this can help you manage your credit card better.

Knowing what the charge represents stops unnecessary worries. It also prepares you to handle your finances with more confidence.

What Ibila Charge Means

An Ibila charge usually refers to a transaction made through a payment processor named Ibila. This name may appear on your statement instead of the actual store or service. Ibila acts as a middleman for many businesses and online purchases.

Because of this, the charge might not look familiar. The merchant’s real name may be different from what shows on your credit card bill. The charge is legitimate but may be listed under the payment processor’s name.

Common Reasons For Ibila Charges

Many Ibila charges come from online shopping or subscription services. These businesses use Ibila to handle payments safely and quickly. Sometimes, you might not remember signing up for these services.

Another reason for an Ibila charge is recurring payments. Subscriptions for apps, memberships, or digital products often renew automatically. The charge date might surprise you if you forgot about the service.

Occasionally, Ibila charges may appear due to shared accounts or family members using your card. It is good to check with others who have access to your credit card. Always review your credit card statements regularly to spot unfamiliar charges early.

Identifying Ibila Charges

Ibila charges can sometimes appear on your credit card without clear details. Knowing how to identify these charges helps you avoid confusion and potential fraud. This section guides you through spotting Ibila charges and understanding the variations in merchant names.

How To Spot Ibila On Statements

Ibila charges may show up under different names on your credit card statement. Check the date and amount carefully. Look for any unfamiliar or repeated entries labeled with “Ibila.” Sometimes, the description might include additional numbers or letters. These help banks track transactions but can make it hard to recognize the charge at first.

Compare the charge with your recent purchases. Think about any subscriptions or services you may have used. If the charge does not match anything you remember, note it for further investigation. Keep your statement details handy when contacting your card issuer.

Merchant Name Variations

Ibila charges can appear with different merchant names. This depends on how the payment processor records the transaction. Names might include variations like “Ibila Pay,” “Ibila Services,” or “Ibila Transactions.” These small changes can confuse cardholders.

Some merchants use third-party processors, which change the name on your statement. This is common with online purchases or subscription services. Always check for similar names that might relate to Ibila. Understanding these variations helps you identify legitimate charges versus unauthorized ones.

Steps To Take If Unfamiliar

Unfamiliar charges on your credit card can cause worry. Act quickly and carefully to handle them. Knowing the right steps helps protect your money and credit score. Follow these steps below to address any unknown Ibila charges.

Review Transaction Details

Check the date, amount, and merchant name on the charge. The merchant name may look different from the store name. Think about recent purchases or subscriptions you might have forgotten. Sometimes, family members use the card with permission. Confirm these details before taking further action.

Contacting The Merchant

Reach out to the merchant listed on your statement. Ask for information about the charge and transaction date. Explain that you do not recognize the charge. The merchant may provide proof of purchase or cancel the transaction. Keep a record of all your communication for reference.

Notifying Your Card Issuer

Call the customer service number on the back of your credit card. Report the unfamiliar charge immediately. Your card issuer can block your card to prevent more unauthorized charges. They will start an investigation and may issue a refund. Follow their instructions carefully and provide all requested information.

Handling Unauthorized Charges

Handling unauthorized charges on your credit card is crucial to protect your finances. These charges can appear without your approval. Acting quickly can limit your loss and fix errors fast.

Understanding how to spot and handle these charges helps you stay safe. This section explains key steps to manage unauthorized charges effectively.

Recognizing Fraudulent Activity

Look at your credit card statement regularly. Check each charge for unfamiliar names or amounts. Fraudulent charges often have odd amounts or come from unknown merchants.

Be alert for multiple small charges. Scammers test cards with small amounts first. Strange patterns or repeated charges should raise a red flag. Early detection helps stop bigger problems.

Filing A Dispute

Contact your credit card issuer immediately if you find a suspicious charge. Use the phone number on the back of your card. Explain the charge you did not make.

Provide details like transaction date, amount, and merchant name. Your issuer will open an investigation. Keep records of all communication for reference.

Chargeback Process

A chargeback lets you reverse an unauthorized transaction. Your credit card company requests money back from the merchant. This process protects you from fraud.

Chargebacks take time, usually a few weeks. Stay in touch with your issuer for updates. Follow their instructions carefully to complete the process smoothly.

Consumer Protection Laws

Consumer protection laws shield you from unfair credit card charges. They help solve disputes and limit your liability for unauthorized transactions.

Understanding these laws can save you money and stress. They provide clear rules for handling errors and fraud on your credit card.

Fair Credit Billing Act

The Fair Credit Billing Act (FCBA) protects consumers from billing errors on credit cards. It covers unauthorized charges, incorrect amounts, and goods not received.

You must report errors within 60 days of the statement date. The card issuer then has 90 days to investigate and fix the issue.

Under FCBA, your liability for unauthorized charges is limited to $50. Many card companies offer zero-liability policies.

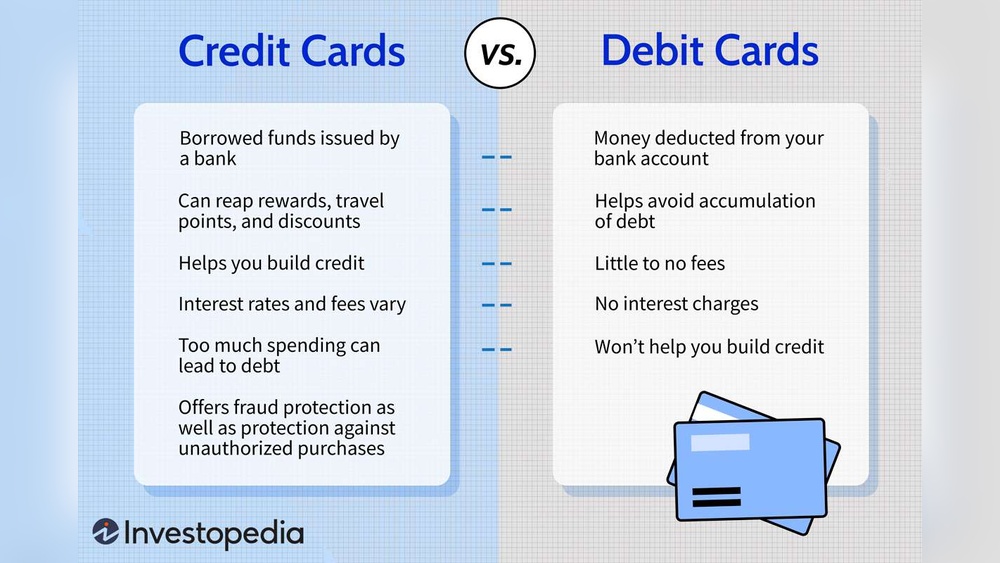

Differences Between Credit And Debit Cards

Credit cards and debit cards offer different protections under the law. Credit cards have stronger safeguards against fraud.

Debit cards link directly to your bank account, so fraud can affect your available funds immediately. Credit cards use a line of credit.

Under federal law, debit card fraud must be reported quickly to limit losses. Credit cards often offer more time to dispute charges.

Knowing these differences helps you choose the best payment method for your situation.

Preventing Future Issues

Preventing future issues with Ibila charges on your credit card saves time and stress. Staying proactive helps catch mistakes early and stops fraud quickly. Taking simple steps protects your money and personal data effectively.

Monitoring Your Statements

Check your credit card statements every month. Look for any charges you do not recognize. Early detection helps stop unauthorized spending fast. Keep a record of your usual purchases for comparison. This habit reduces the chance of missed fraud or errors.

Setting Up Alerts

Most credit card companies offer alerts by text or email. Set alerts for every transaction or for large amounts. Alerts notify you immediately about new charges. This instant update helps you act quickly if something looks wrong. Use your bank’s app or website to turn alerts on.

Securing Your Credit Card Information

Keep your credit card details safe and private. Do not share your card number or PIN with others. Avoid using public Wi-Fi when shopping online. Use strong passwords for accounts linked to your credit card. Regularly update your passwords to add extra security.

Frequently Asked Questions

What’s That Charge On My Credit Card?

Check your credit card statement for transaction details and merchant name. Contact the merchant if needed. Report unknown or suspicious charges to your card issuer immediately. They will investigate and may issue a refund if the charge is unauthorized or incorrect.

How Do I Find Out Where A Charge Came From On My Credit Card?

Review your credit card statement for merchant details and transaction date. Contact the merchant if unclear. Call your card issuer to report unknown charges and dispute if necessary. Keep records of all communications for follow-up.

Why Am I Getting Random Charges On My Credit Card?

Random credit card charges often result from unauthorized use, subscription renewals, or merchant billing errors. Review statements carefully and contact your card issuer immediately to dispute suspicious transactions.

What If I Don’t Recognize A Charge On My Card?

Check the transaction details carefully to confirm unfamiliarity. Contact your card issuer immediately to report suspicious charges. They will investigate and may refund you if fraud occurs. Keep records of all communications for follow-up. Acting quickly helps protect your account and prevent further unauthorized use.

Conclusion

Understanding the Ibila charge on your credit card helps you manage your finances better. Always check your statement carefully for unfamiliar transactions. If you see a charge you don’t recognize, act quickly by contacting your card issuer. Keep your information safe to avoid unauthorized charges.

Staying informed protects your credit and peace of mind. Remember, taking simple steps can prevent future issues with your credit card.