Your credit score holds the key to unlocking better loan rates, credit cards, and even rental opportunities. But have you ever wondered how this magical number is actually calculated?

Understanding what goes into your credit score can help you take control of your financial future. You’ll discover the simple factors that shape your score, how lenders see your creditworthiness, and practical tips to improve your number. Keep reading to learn exactly what impacts your credit score and how you can boost it to open new doors.

Credit Score Basics

Understanding credit score basics helps you see how lenders decide your creditworthiness. A credit score is a number that shows how likely you are to pay back borrowed money. It plays a key role in getting loans, credit cards, and even renting homes.

What Credit Scores Represent

Credit scores represent your financial trustworthiness. They show lenders your history of borrowing and repaying money. A high score means you manage credit well and pay bills on time. A low score may suggest risk or missed payments. Scores usually range from 300 to 850. The higher the score, the better your credit status.

Major Credit Bureaus

Three main credit bureaus collect and store your credit information. They are Experian, Equifax, and TransUnion. These agencies get data from banks, credit card companies, and other lenders. Each bureau creates a credit report based on this data. Lenders use these reports to calculate your credit score. Scores may vary slightly between bureaus due to different data.

Key Credit Scoring Models

Credit scores are essential for financial decisions. Various models calculate these scores. Each model uses specific rules and data. Understanding these models helps you manage your credit better.

Two main credit scoring models dominate the market. The FICO Score and VantageScore. Both are widely used by lenders to assess credit risk. They consider similar factors but weigh them differently.

Fico Score Explained

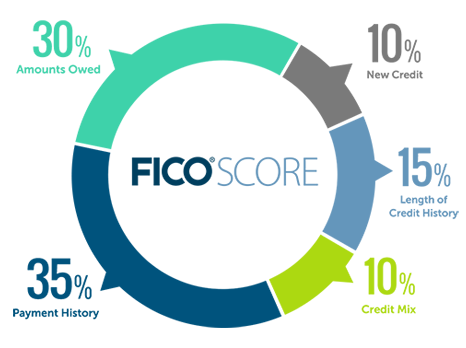

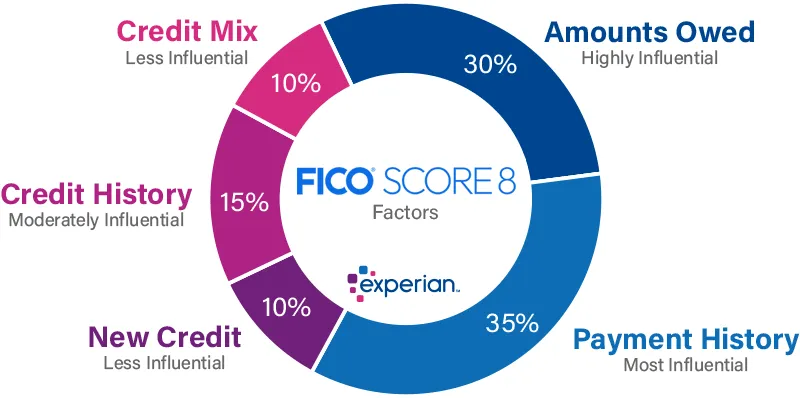

The FICO Score is the most common credit score. It ranges from 300 to 850 points. This score is based on five key factors.

- Payment history (35%): Shows if you pay bills on time.

- Amounts owed (30%): The total debt you owe versus credit limits.

- Length of credit history (15%): How long you have had credit accounts.

- New credit (10%): Recent credit inquiries and new accounts.

- Credit mix (10%): Variety of credit types like cards and loans.

FICO updates its scoring models regularly. Different versions may be used depending on the lender. This score helps lenders predict your likelihood to repay loans.

Vantagescore Overview

VantageScore is a newer model created by the three major credit bureaus. It also scores from 300 to 850. This model uses similar factors but with some differences.

- Payment history: Most important factor, like FICO.

- Age and type of credit: Considers how long accounts have been open and their types.

- Credit utilization: How much of your available credit you use.

- Total balances: The total amount you owe across all accounts.

- Recent credit behavior: Looks at new accounts and inquiries.

VantageScore can score people with less credit history. It updates more frequently than some FICO versions. Many lenders now accept VantageScore alongside FICO scores.

Payment History Impact

Payment history plays a major role in calculating credit scores. It shows how well you manage your debts over time. Lenders check this history to decide if you are a reliable borrower. A solid record of timely payments builds trust and improves your score.

On-time Payments

Making payments on or before the due date helps your credit score. Each on-time payment proves you can handle credit responsibly. Consistent on-time payments show lenders that you respect your financial commitments. This positive record can raise your credit score steadily.

Late Payments And Defaults

Late payments lower your credit score significantly. The longer the delay, the bigger the negative impact. Defaults and missed payments stay on your report for years. They signal risk to lenders, making it harder to get new credit. Avoiding late payments protects your credit health.

Credit Utilization Ratio

The credit utilization ratio plays a key role in credit score calculations. It shows how much credit you use compared to your total credit limit. This ratio helps lenders see if you rely too much on borrowed money. Keeping this ratio low suggests you manage credit well. A high ratio may signal financial stress and lower your score.

Calculating Utilization

To calculate credit utilization, divide your total credit card balances by your total credit limits. For example, if your balance is $500 and your limit is $2,000, your utilization ratio is 25%. Lenders prefer to see a utilization ratio below 30%. This number is calculated for each card and across all cards combined.

Effects On Scores

Credit utilization directly impacts your credit score. Lower utilization often leads to higher scores. High utilization can lower your score, even with on-time payments. Scores can drop quickly if you max out cards. Regularly paying down balances helps maintain a healthy ratio. This shows lenders you use credit responsibly and can manage debt.

Length Of Credit History

The length of your credit history plays a key role in calculating your credit score. It shows how long you have used credit and how well you manage it over time. Lenders prefer borrowers with a longer credit history because it helps predict future behavior. This factor looks at several details about your accounts to assess your credit experience.

Average Account Age

Average account age means the average time your credit accounts have been open. Older accounts increase your average age and boost your score. New accounts lower the average age and may reduce your score. Keeping old accounts open helps maintain a higher average age. This shows lenders you have a longer, stable credit history.

Recent Activity

Recent activity means how often you open or close accounts. Opening many new accounts in a short time lowers your score. Closing older accounts can also reduce your average account age. Lenders see frequent changes as riskier behavior. It is better to avoid opening or closing accounts too quickly.

Credit: www.ssbpgh.com

Types Of Credit Accounts

Credit scores depend on the types of credit accounts you hold. These accounts show lenders how you manage different kinds of debt. The variety and management of these accounts impact your score.

Revolving Vs. Installment

Revolving accounts let you borrow up to a limit and repay over time. Credit cards are the most common type. You can carry a balance or pay it off monthly.

Installment accounts have a fixed loan amount. You pay set monthly payments until the loan ends. Examples include car loans and mortgages.

Both types affect your credit score. Keeping balances low on revolving accounts helps. Making on-time payments on installment loans builds trust.

Mix And Diversity

Credit scoring models like to see a mix of account types. It shows you can handle different debts responsibly. A good mix may improve your credit score.

Having only one type of account might limit your score potential. For example, only credit cards or only loans. Lenders prefer borrowers who manage varied credit well.

Try to maintain a healthy balance of revolving and installment accounts. This mix demonstrates financial flexibility and reliability. It can make your credit profile stronger.

New Credit Inquiries

New credit inquiries happen when lenders check your credit report. These checks occur when you apply for a new loan or credit card. Each inquiry provides information about your recent credit activity. This information helps lenders decide if they should approve your application. Understanding how these inquiries affect your credit score is important. It can help you manage your credit better.

Hard Vs. Soft Inquiries

Hard inquiries happen when a lender reviews your credit for a loan or credit card. These inquiries can lower your credit score slightly. They stay on your credit report for about two years. Soft inquiries do not affect your credit score. These happen when you check your own credit or when a company pre-approves you for an offer. Only hard inquiries impact your credit score.

Impact Of Multiple Applications

Applying for many credit accounts in a short time can hurt your score. Each hard inquiry adds a small risk to your credit profile. Too many inquiries suggest higher risk to lenders. Credit scoring models may group similar inquiries for the same type of loan. This means multiple inquiries in a short period may count as one. Still, multiple applications over time can lower your credit score.

Income And Debt Ratios

Income and debt ratios play a key role in credit score calculations. These ratios show how much money you earn versus how much you owe. Lenders use this information to decide if you can handle more credit. Understanding these ratios helps you manage your finances better. It also improves your chances of getting approved for loans or credit cards.

Debt-to-income Ratio Role

The debt-to-income (DTI) ratio compares your monthly debts to your monthly income. A lower DTI ratio means you have more income left after paying debts. Lenders prefer borrowers with low DTI because they are less risky. A high DTI ratio suggests you might struggle to make payments on new loans. Keeping your DTI below 36% is ideal for good credit health.

Income Considerations

Income affects your ability to repay debts but does not directly impact your credit score. Lenders review your income to ensure you can cover monthly payments. Stable and consistent income improves your loan approval chances. Changes in income might affect your borrowing limits. Always report accurate income information when applying for credit.

Data Collection Process

The data collection process plays a vital role in how credit scores are calculated. It involves gathering accurate and timely information about your credit behavior. This data comes from various sources, mainly lenders and credit bureaus. Without this information, credit scores could not reflect your true creditworthiness.

Credit bureaus collect data regularly to keep credit reports up to date. The process starts with lenders reporting your credit activity. This includes details about your loans, credit cards, payment history, and balances. The quality and accuracy of this data directly affect your credit score.

Reporting By Lenders

Lenders send information about your credit accounts to credit bureaus. This report usually happens every month. They include data such as payment status, credit limits, and outstanding balances. Lenders report both positive and negative details. For example, late payments or defaults are also shared. This helps credit bureaus maintain a full picture of your credit behavior.

Not all lenders report to every credit bureau. Some may report to only one or two. This can cause differences in credit reports from each bureau. Still, most major lenders participate in this reporting process. It keeps your credit file current and comprehensive.

Credit Report Compilation

Credit bureaus collect all the data from various lenders. They organize this information into your credit report. The report lists your credit accounts, payment history, inquiries, and public records. It serves as the basis for calculating your credit score.

The bureaus check the data for accuracy and consistency. They remove duplicate or incorrect entries. The updated report reflects your current credit status. Credit scoring models then use this report to generate your score. This process repeats regularly to ensure your credit score stays relevant.

Credit: www.experian.com

Improving Your Credit Score

Improving your credit score takes steady effort and smart choices. Small changes in how you handle credit can boost your score over time. Focus on key areas that lenders value most. These actions help build trust with credit agencies. Here are three important ways to improve your credit score.

Timely Payments

Paying bills on time is the most important step. Late or missed payments lower your credit score quickly. Set reminders or automatic payments to avoid delays. Consistent, timely payments show you handle credit responsibly. This builds a positive payment history, which lenders prefer.

Reducing Debt Balances

Lower your overall debt to improve your credit score. High balances on credit cards can harm your score. Aim to keep your credit card balances below 30% of the limit. Paying down debt reduces your credit utilization ratio. This ratio is a key factor in credit scoring models.

Managing Credit Applications

Limit the number of new credit applications you make. Each application can cause a small, temporary drop in your score. Multiple applications in a short time raise red flags for lenders. Only apply for credit when necessary and space out your requests. This helps maintain a stable credit profile.

Credit: www.rundeautogroup.com

Frequently Asked Questions

How To Get A 700 Credit Score In 30 Days?

Pay all bills on time, reduce credit card balances below 30%, avoid new credit inquiries, and correct errors on your credit report.

What Credit Score Do You Need For A $400,000 House?

A credit score of at least 620 is typically needed to qualify for a $400,000 house loan. Higher scores get better rates. Lenders also consider income, debts, and down payment size. Aim for 700+ for optimal mortgage offers and lower interest rates.

What Is The Credit Card Limit For $70,000 Salary?

A $70,000 salary may qualify for a credit card limit between $7,000 and $21,000. Lenders consider credit history and debt-to-income ratio. Strong credit and low debts can increase your limit. Card type also influences the starting limit.

What Makes Up 30% Of Your Credit Score?

Payment history makes up 30% of your credit score. It reflects timely bill payments and missed payments.

Conclusion

Understanding how credit scores are calculated helps you manage your finances better. Payment history, credit usage, account types, and recent activity all matter. Keeping balances low and paying bills on time improves your score. Regularly checking your credit report can catch errors early.

A good score opens doors to better loan options and rates. Stay informed and make smart credit choices for a healthier financial future.