How much should you save each month to feel secure and reach your financial goals? It’s a question many ask but few answer with confidence.

The truth is, there’s no one-size-fits-all number. Your ideal savings amount depends on your income, expenses, and future plans. But what if you had expert advice tailored to your situation? Imagine turning your paycheck into a powerful tool that builds your safety net and opens doors to new opportunities.

You’ll discover simple, practical strategies to decide exactly how much you should save monthly — and how to make saving a habit that sticks. Ready to take control of your financial future? Let’s dive in.

Monthly Savings Benchmarks

Knowing how much to save each month can be confusing. Monthly savings benchmarks help you set clear goals. These guidelines consider your income, age, and life stage. They make saving more practical and achievable.

Use these benchmarks as a starting point. Adjust them based on your personal needs and financial situation. The key is consistency and steady progress.

General Rules Of Thumb

Many experts suggest saving at least 20% of your monthly income. This includes money for emergencies and future goals. If 20% is not possible, start with a smaller amount. Increase your savings little by little over time. The important part is to save regularly.

Savings By Income Level

Your income affects how much you can save each month. Higher earners may save a larger percentage. Lower earners might save less but still make progress. Aim to save a fixed amount or percentage each month. This habit builds financial security regardless of income.

Adjusting For Age And Life Stage

Saving needs change as you age. Younger people can save less but start early. Middle-aged savers should increase contributions for retirement. Older adults focus on preserving savings and managing expenses. Adjust your savings plan to fit your current life stage. This keeps your goals realistic and reachable.

Credit: www.chegg.com

Setting Realistic Savings Goals

Setting realistic savings goals is key to managing your money well. Clear goals help you stay focused and motivated. They also make saving less stressful and more achievable. Knowing what you want to save for guides your monthly savings amount. It is important to balance your needs and your income to set goals that work for you.

Start by identifying the time frame and purpose for your savings. Short-term and long-term goals require different plans. Prioritize your goals based on your current situation and future plans. This approach helps you create a savings strategy that fits your life.

Short-term Vs Long-term Goals

Short-term goals are things you want soon. Examples include a vacation, new phone, or holiday gifts. These goals usually need money saved within a year or two. Long-term goals take more time and money. Buying a house or paying for education are common long-term goals. Knowing the difference helps you decide how much to save monthly. Save more for long-term goals by starting early. For short-term goals, save smaller amounts but stay consistent.

Emergency Fund Targets

An emergency fund is money set aside for unexpected costs. This fund protects you from financial trouble during job loss or illness. Experts suggest saving three to six months’ worth of expenses. Calculate your monthly essential expenses to find your target amount. Build this fund first before other goals. Save a small portion of your income each month until you reach your target. This fund gives you peace of mind and financial security.

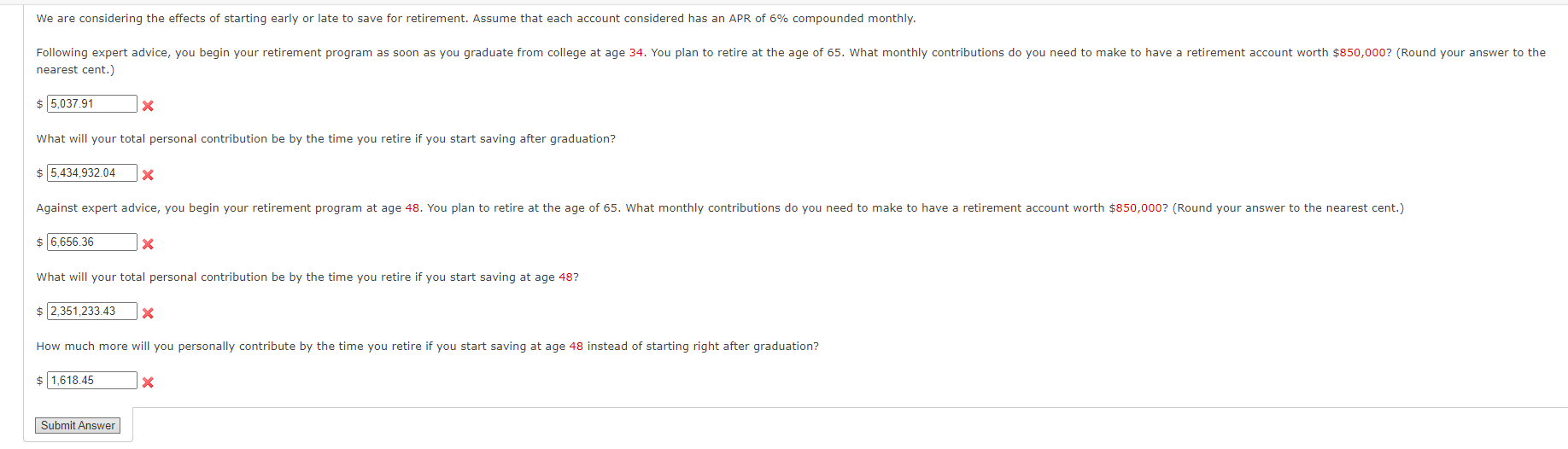

Retirement Planning Savings

Retirement planning means saving money for your life after work. Start saving early to benefit from compound interest. Experts recommend saving at least 15% of your income for retirement. Use retirement accounts or employer plans to grow your savings. Adjust your monthly savings as your income changes. Consistent saving ensures you have enough money to live comfortably later.

Income And Expense Assessment

Understanding your income and expenses is the first step to saving money wisely. Assessing these two factors helps you create a realistic savings plan. This section guides you through tracking income, analyzing spending, and finding extra money to save.

Tracking Monthly Income

Start by listing all your income sources. Include your salary, freelance work, and any side jobs. Don’t forget bonuses, gifts, or other irregular earnings. Knowing your total monthly income sets the base for your savings goal. Use a notebook or a budgeting app to keep records. Consistent tracking ensures you know exactly how much money you have each month.

Analyzing Spending Patterns

Review your monthly expenses carefully. Categorize them into needs and wants. Needs include rent, utilities, and groceries. Wants cover dining out, entertainment, and shopping. Spot where most of your money goes. Look for areas where you can cut back. Understanding your spending helps you decide how much to save. Track your expenses for at least a month for accuracy.

Identifying ‘found Money’

‘Found money’ means extra cash you can save easily. This might be money saved by canceling unused subscriptions. Or it could be discounts and cashback offers. Sometimes, small changes like cooking at home save money. These savings add up over time. Add this ‘found money’ to your monthly savings. It boosts your savings without affecting your lifestyle.

Credit: www.annuityexpertadvice.com

Smart Budgeting Techniques

Smart budgeting techniques help you control your money better. They guide you to save a set amount every month. Using simple methods makes budgeting less confusing. These techniques fit different lifestyles and income levels. You can choose one that works best for your needs. Let’s explore some popular budgeting methods.

Zero-based Budgeting

Zero-based budgeting assigns every dollar a job. You plan your income minus expenses to equal zero. This means you know exactly where your money goes. It helps prevent overspending and encourages saving. Start by listing all income and all expenses. Adjust until your income minus expenses equals zero. This method forces you to think about saving each month.

50/30/20 Rule

The 50/30/20 rule divides income into three parts. Use 50% for needs like rent and bills. Spend 30% on wants like dining out or hobbies. Save 20% for future goals and emergencies. This simple rule balances spending and saving. It gives you flexibility while keeping savings steady. Many find this rule easy to follow and effective.

Cutting Non-essential Expenses

Cutting non-essential expenses frees up money for savings. Look at your spending and spot things you do not need. Cancel unused subscriptions and avoid impulse buys. Cook meals at home instead of dining out often. Small cuts add up quickly and boost your monthly savings. Track spending carefully to find areas to reduce.

Automating Your Savings

Automating your savings removes the stress of manual transfers. It builds steady saving habits without daily effort. Setting up automatic savings helps you stay consistent and reach your goals faster.

Setting Up Automatic Transfers

Start by linking your checking and savings accounts. Choose a fixed amount to transfer every payday. This ensures your savings grow regularly without extra work. Adjust the amount as your income or goals change.

Choosing High-interest Accounts

Pick a savings account that offers a good interest rate. Higher interest means your money grows faster over time. Look for online banks or credit unions with competitive rates. This boosts your savings without extra deposits.

Pay Yourself First Strategy

Make savings your top priority each month. Treat your savings like a bill that must be paid. Transfer money to your savings before spending on anything else. This habit protects your savings from being spent.

Maximizing Savings Growth

Growing your savings effectively takes more than just putting money aside. It requires smart choices about where and how to save. Maximizing savings growth means using tools and accounts that help your money earn more over time. This approach helps you reach your financial goals faster and with less effort. Small monthly savings add up better when they work hard for you.

High-yield Savings Options

High-yield savings accounts offer higher interest rates than regular accounts. They let your money grow faster without risk. Many banks and online lenders provide these accounts. Look for accounts with no fees and easy access to your money. This option is great for short-term savings or emergency funds.

Investing For Long-term Growth

Investing can increase your savings more than a bank account. Stocks, bonds, and mutual funds provide higher returns over many years. Investing carries some risk, but long-term growth often beats inflation. Start with small amounts and increase as you learn more. Diversify your investments to reduce risk and improve stability.

Tax-advantaged Accounts

Tax-advantaged accounts help your savings grow faster by reducing taxes. Examples include IRAs, 401(k)s, and HSAs. Money grows tax-free or tax-deferred in these accounts. Use them to save for retirement or medical costs. Check limits and rules to maximize their benefits. These accounts add extra value to your monthly savings.

Handling Financial Setbacks

Financial setbacks can disrupt your saving plans. Life is unpredictable. Emergencies like job loss, medical bills, or urgent repairs can demand immediate cash. Handling these situations carefully helps you stay on track with your long-term savings goals. Knowing how to adjust during tough times prevents added stress and financial damage.

Adjusting Savings During Emergencies

Pause or reduce your monthly savings if an emergency arises. Focus on covering essential expenses first. Use your emergency fund to avoid debt. If you don’t have one, try saving smaller amounts until you recover. Resume normal savings once your situation stabilizes. This flexible approach keeps your finances balanced.

Debt Repayment Vs Savings Balance

High-interest debt should take priority over saving. Paying off debt reduces financial strain faster. Avoid accumulating more debt during setbacks. After clearing urgent debts, rebuild your savings gradually. Balance both goals by allocating funds wisely. This strategy protects your financial health in the long run.

Reevaluating Goals Periodically

Review your savings goals every few months. Life changes may require adjusting targets or timelines. Update your budget to match current income and expenses. Set realistic goals based on your new situation. Regular check-ins help maintain motivation and focus. Flexibility is key to managing finances successfully.

Expert Tips And Tools

Saving money every month can feel confusing without clear guidance. Experts suggest practical tips and tools to make saving easier. Using the right resources helps you set realistic goals and track progress. Below are some expert tips and tools to guide your monthly savings plan.

Using Savings Calculators

Savings calculators help estimate how much to save monthly. Enter your income, expenses, and goals. The calculator shows how long it takes to reach your target. It adjusts based on interest rates and inflation. These tools give a clear saving plan. You can find many free calculators online.

Financial Advisor Insights

Financial advisors offer personalized advice for saving money. They consider your income, debts, and future plans. Advisors suggest saving a certain percentage of your income. Many recommend saving at least 20% monthly. They help balance saving with spending needs. Talking with an advisor can improve your money habits.

Apps To Track And Boost Savings

Saving apps make managing money simple and visual. These apps track spending and show how much you can save. Some apps round up purchases and save the difference. Others help create budgets and send saving reminders. Using apps keeps your savings goal in focus. They work well for beginners and experienced savers alike.

Credit: shop.chessbase.com

Frequently Asked Questions

What Is The $27.40 Rule?

The $27. 40 rule suggests saving $27. 40 daily to build a $10,000 emergency fund in one year. It promotes consistent, manageable saving habits.

How Much Money Do Financial Experts Recommend You Save?

Financial experts recommend saving at least 20% of your monthly income. Aim to build an emergency fund covering 3-6 months of expenses. Consistent saving habits secure financial stability and future goals. Automate savings and adjust budgets to meet these targets effectively.

What Is The 70/30/10 Rule Money?

The 70/30/10 money rule divides income into 70% for needs, 30% for wants, and 10% for savings or debt repayment.

What Is The $1000 A Month Rule?

The $1000 a month rule suggests saving $1000 monthly to build emergency funds and achieve financial goals quickly. Automate savings to stay consistent and treat it as a fixed expense. This rule helps develop disciplined saving habits and financial security over time.

Conclusion

Saving money each month builds financial security step by step. Start small and increase savings as your income grows. Automate transfers to make saving easier and consistent. Track your spending and adjust your budget to find extra savings. Treat your savings like a monthly bill you must pay.

Over time, these habits create a strong financial cushion. Remember, saving is a personal journey—find what works best for you. Stay patient and focused on your goals. Small efforts today lead to greater peace tomorrow.