Have you ever wondered how money might change in the future? Central Bank Digital Currencies, or CBDCs, are becoming a hot topic that could reshape the way you use cash and make payments.

But what exactly are CBDCs, and why should you care about them? Understanding these digital currencies can help you stay ahead in a world that’s quickly moving toward new financial technology. Keep reading to discover how CBDCs might impact your wallet, your privacy, and the economy around you.

Credit: bitcoin.tax

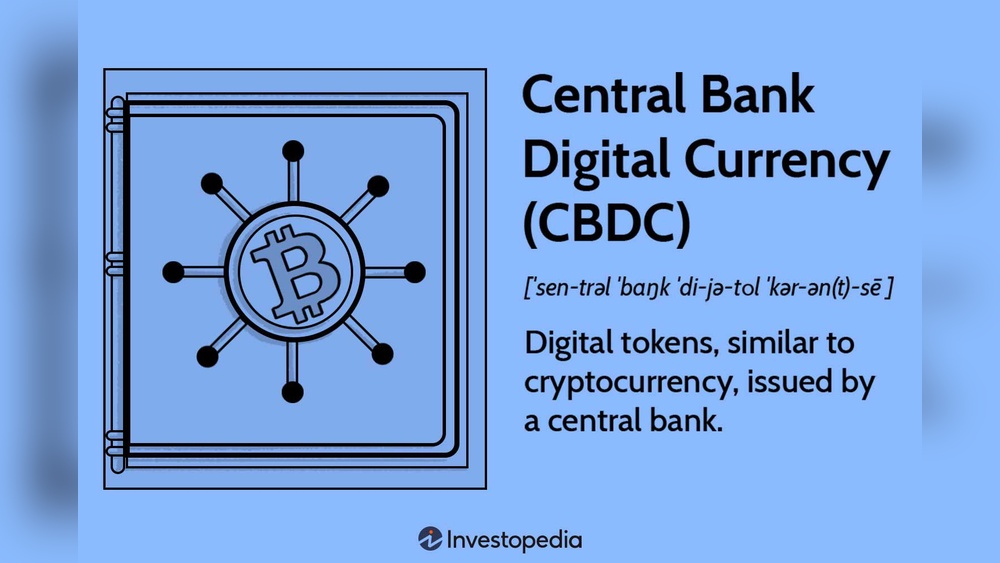

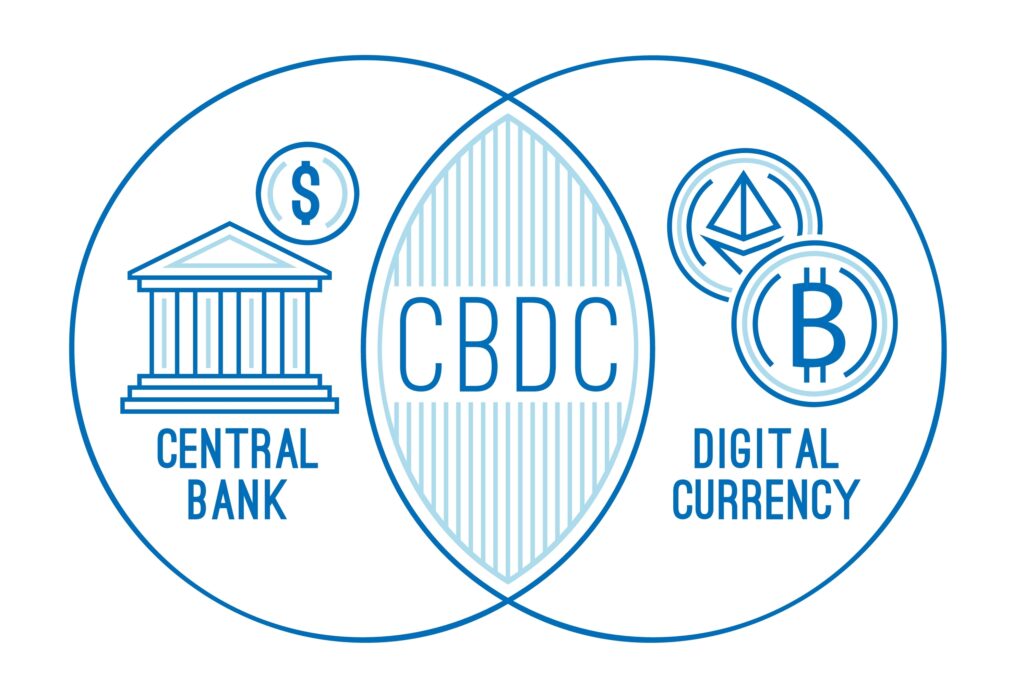

What Are Cbdcs

Central Bank Digital Currencies, or CBDCs, are a new form of money. They are digital versions of a country’s official currency. Unlike cash or coins, CBDCs exist only in electronic form. Many countries explore CBDCs to improve payments and banking systems.

Understanding what CBDCs are helps grasp their growing importance. They offer a way to make digital money safe and easy to use for everyone.

Definition And Basics

CBDCs are digital currencies issued by a country’s central bank. They represent the same value as physical money. People can use them to pay for goods and services. CBDCs are backed by the government, ensuring trust and stability.

Unlike private digital money, CBDCs have official status. They aim to make payments faster and cheaper. Central banks control CBDCs to manage the economy better.

How Cbdcs Differ From Cryptocurrencies

CBDCs are not the same as cryptocurrencies like Bitcoin. Cryptocurrencies are decentralized and operate without a central authority. CBDCs are centralized and regulated by governments.

Cryptocurrencies can be very volatile in price. CBDCs maintain a stable value like regular money. This makes CBDCs safer for everyday use.

CBDCs also follow strict rules to prevent illegal activities. Cryptocurrencies can be harder to regulate and track.

Types Of Cbdcs

There are two main types of CBDCs: retail and wholesale. Retail CBDCs are for the general public. People can use them for daily transactions, like buying groceries.

Wholesale CBDCs are for banks and financial institutions. They help with large transactions and clearing payments quickly. Both types aim to improve the financial system’s efficiency.

Credit: trendsresearch.org

Benefits Of Cbdcs

Central Bank Digital Currencies (CBDCs) offer many benefits for both individuals and the economy. They can change how money works in daily life and across financial systems. CBDCs aim to make payments faster, cheaper, and more accessible. They also help governments manage money better.

Enhanced Payment Efficiency

CBDCs allow instant money transfers. Payments happen in seconds, not days. This speed helps businesses and people save time. It also reduces errors common in traditional payments. Faster payments mean easier access to money anytime.

Financial Inclusion

Many people lack access to banks or digital payment tools. CBDCs provide a safe way to store and use money without a bank account. They can reach rural or poor areas with limited banking services. This inclusion helps more people join the economy.

Reduced Transaction Costs

CBDCs cut down fees for payments and transfers. No need for middlemen like banks or payment processors. Lower costs benefit consumers and businesses. Saving on fees means more money stays in your pocket.

Improved Monetary Policy Implementation

Governments can use CBDCs to control money supply better. They can track how money moves in the economy. This helps in making policies that support growth and stability. It also reduces risks like inflation or deflation.

Risks And Challenges

Central Bank Digital Currencies (CBDCs) offer many benefits but also come with risks and challenges. These issues need careful thought before adoption. Understanding these risks helps prepare for the future.

Privacy Concerns

CBDCs could track every transaction users make. This raises worries about personal data being monitored by governments or other entities. People may lose control over their financial privacy. Ensuring user anonymity while preventing crime is a tough balance.

Cybersecurity Threats

Digital currencies depend on secure technology. Cyberattacks could steal funds or disrupt systems. Hackers might target the central bank or users. Constant updates and strong defenses are needed to protect the network.

Impact On Banks And Financial Stability

CBDCs might reduce the need for traditional banks. People could keep money directly with the central bank. This could hurt banks’ ability to lend and operate. It may also affect the overall financial system’s stability.

Technical And Regulatory Hurdles

Building a CBDC requires advanced technology and infrastructure. Different countries have various rules and regulations. Coordinating these is complex and time-consuming. Clear laws and smooth technology must work together for success.

Credit: sdk.finance

Global Cbdc Developments

Central Bank Digital Currencies (CBDCs) are gaining attention worldwide. Countries explore them to improve payment systems and financial inclusion. Many nations run projects to test CBDCs. These efforts shape the future of money and banking.

Leading Countries And Projects

China leads with its digital yuan, widely tested across cities. The European Central Bank studies a digital euro for the Eurozone. The Bahamas launched the Sand Dollar, the first fully live CBDC. Other countries like Sweden and Canada also explore digital currency pilots. Each project targets specific local needs and goals.

International Collaboration

Central banks share knowledge and experiences on CBDC development. Groups like the Bank for International Settlements support cooperation. This helps harmonize standards and avoid risks in cross-border payments. Joint research improves security and privacy features. Collaboration speeds up learning and reduces costly mistakes.

Lessons From Pilot Programs

Pilot programs reveal technical challenges and user behavior insights. They test system resilience against cyber threats. Feedback shows how citizens use and accept digital money. Many pilots highlight the need for clear regulation and public trust. Lessons guide safer and more effective CBDC designs worldwide.

Why Cbdcs Matter Now

Central Bank Digital Currencies (CBDCs) are becoming important today. They offer a new way to use money in digital form. Many countries explore CBDCs to keep up with changes in technology and society.

CBDCs could change how people pay for goods and services. They provide a safe and easy way to handle money without cash or cards. The shift to digital money affects banks, businesses, and everyday users.

Digital Transformation Of Money

Money is moving from physical to digital forms. Smartphones and the internet make digital payments popular. CBDCs help central banks create money that works well in this digital world. They offer a secure way to use digital money backed by the government.

This change helps reduce fraud and speed up transactions. It also makes sending money across borders easier and cheaper.

Response To Declining Cash Usage

Cash use is falling in many countries. People prefer cards and mobile payments. Some places even plan to stop using cash entirely. CBDCs provide a digital alternative that keeps money accessible to everyone.

They help those who do not have bank accounts but use smartphones. CBDCs can make payments simple and reach more people safely.

Geopolitical And Economic Factors

Countries want to keep control over their money systems. CBDCs help protect economies from outside risks. They allow governments to monitor and manage money flows better.

CBDCs can reduce the power of foreign currencies in domestic markets. This helps strengthen national financial stability and independence.

Future Of Payments And Finance

CBDCs shape the future of how people pay and save money. They support faster, cheaper, and safer transactions. Banks and businesses can build new services on top of CBDCs.

They also open doors for innovations like smart contracts and programmable money. CBDCs prepare economies for a world that relies more on digital finance.

Frequently Asked Questions

What Are Central Bank Digital Currencies (cbdcs)?

CBDCs are digital forms of a country’s official currency issued by the central bank. They aim to provide a secure and efficient payment method. Unlike cryptocurrencies, CBDCs are regulated and backed by the government, ensuring stability and trust for users.

How Do Cbdcs Differ From Cryptocurrencies?

CBDCs are government-issued and regulated digital currencies, while cryptocurrencies are decentralized and unregulated. CBDCs focus on stability and legal tender status, whereas cryptocurrencies prioritize privacy and decentralization. This difference impacts their use, regulation, and adoption worldwide.

Why Are Cbdcs Important For The Economy?

CBDCs enhance payment efficiency, reduce transaction costs, and increase financial inclusion. They provide governments better control over monetary policy and combat fraud. CBDCs also modernize the financial system, supporting innovation and economic growth in a digital age.

Can Cbdcs Replace Cash Entirely?

CBDCs may reduce the need for physical cash but are unlikely to replace it completely soon. Cash remains important for privacy and accessibility. CBDCs complement cash by offering a digital alternative, promoting a hybrid financial ecosystem.

Conclusion

Central Bank Digital Currencies are changing how money works. They offer faster payments and more security. People can use digital money easily and safely. Banks and governments are exploring these new currencies. Understanding CBDCs helps us prepare for the future.

The world’s money system could become simpler and fairer. Keeping an eye on CBDC developments matters for everyone. This digital shift could impact daily life soon. Stay informed and ready for changes ahead.